CEG Set to Report Q2 2025 Earnings

Investors are closely watching this report amid changing dynamics in the energy sector and recent gains in the company’s stock price. Image Source: Zacks Investment ResearchForecasts: Revenue Dip, But Earnings Growth

Image Source: Zacks Investment ResearchForecasts: Revenue Dip, But Earnings Growth

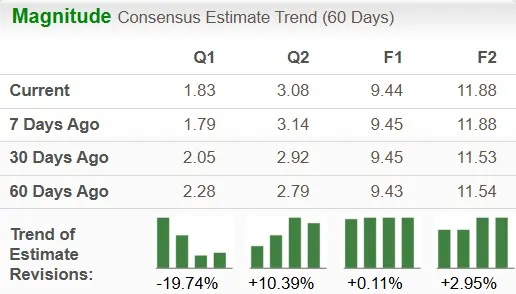

Analysts polled by Zacks have forecasted second-quarter revenues of approximately $5.06 billion for Constellation Energy, which would mark a 7.6% decline compared to the same quarter last year. Despite this drop in sales, earnings are expected to improve. The consensus estimate for earnings per share (EPS) stands at $1.83, signaling an 8.9% increase from the previous year. Image Source: Zacks Investment ResearchHowever, it’s worth noting that this EPS estimate has edged slightly lower over the past 60 days, suggesting that analysts are cautiously adjusting expectations ahead of the report.Earnings Track Record: A Mixed Bag

Image Source: Zacks Investment ResearchHowever, it’s worth noting that this EPS estimate has edged slightly lower over the past 60 days, suggesting that analysts are cautiously adjusting expectations ahead of the report.Earnings Track Record: A Mixed Bag

Over the last four quarters, Constellation Energy has exceeded earnings expectations three times and met once. This track record has delivered an average earnings surprise of 7.41%, reflecting the company's ability to outperform in recent reporting periods.What the Quant Model Suggests

Despite the positive earnings growth outlook, Zacks’ proprietary model doesn’t strongly indicate that Constellation Energy will beat expectations this time around. A combination of a positive Earnings ESP (Expected Surprise Prediction) and a Zacks Rank of #1 (Strong Buy), #2 (Buy), or #3 (Hold) tends to boost the chances of an earnings beat. But in this case, Constellation has an Earnings ESP of 0.00% and currently holds a Zacks Rank #3 (Hold), which does not conclusively tip the odds in favor of a surprise.Sector Peers That Could Outperform

Investors seeking alternatives in the energy space might consider stocks like Permian Resources Corporation (PR), Talos Energy (TALO), and SolarEdge Technologies (SEDG). All three have positive Earnings ESPs—PR at +3.51%, TALO at +34.58%, and SEDG at +4.53%—and currently maintain a Zacks Rank #3. This combination boosts the probability of an earnings beat for these companies.Factors That May Have Driven Q2 Performance

Constellation Energy’s Q2 performance likely benefited from multiple operational tailwinds. Strong commercial execution, customer demand growth, and optimized energy portfolio management are expected to support earnings. Image Source: Zacks Investment ResearchIts extensive nuclear infrastructure plays a key role in meeting the escalating electricity demands of data centers, likely driving revenue stability. The company’s active expansion into renewables, beyond its traditional nuclear focus, also positions it well for sustainable long-term growth.CEG’s emphasis on providing customer-centric, low-carbon solutions—such as carbon-free energy and renewable energy certifications—may further bolster profitability and appeal to clients aiming to reduce emissions and manage energy costs effectively.Stock Performance and Valuation

Image Source: Zacks Investment ResearchIts extensive nuclear infrastructure plays a key role in meeting the escalating electricity demands of data centers, likely driving revenue stability. The company’s active expansion into renewables, beyond its traditional nuclear focus, also positions it well for sustainable long-term growth.CEG’s emphasis on providing customer-centric, low-carbon solutions—such as carbon-free energy and renewable energy certifications—may further bolster profitability and appeal to clients aiming to reduce emissions and manage energy costs effectively.Stock Performance and Valuation

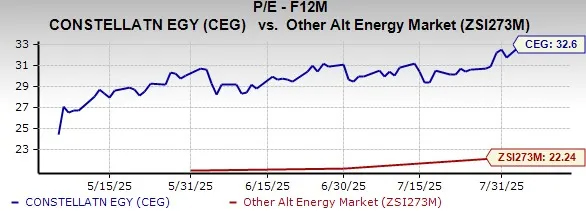

In the last three months, Constellation Energy shares have surged by 29.6%, outpacing the broader industry’s 23.9% gain. This strong rally, however, has pushed the stock to trade at a premium. Image Source: Zacks Investment ResearchCEG’s forward 12-month price-to-earnings (P/E) ratio stands at 32.60x, well above the industry average of 22.24x, reflecting elevated investor expectations and a potential valuation concern for new entrants.Should Investors Buy, Hold, or Wait?

Image Source: Zacks Investment ResearchCEG’s forward 12-month price-to-earnings (P/E) ratio stands at 32.60x, well above the industry average of 22.24x, reflecting elevated investor expectations and a potential valuation concern for new entrants.Should Investors Buy, Hold, or Wait?

Given Constellation Energy’s consistent growth strategies, expanding renewable portfolio, and solid execution, current investors may find it wise to hold the stock through the upcoming earnings report. However, for potential new investors, it may be prudent to wait until after the earnings release before initiating a position—especially considering the stock’s premium valuation and the lack of a strong signal for an earnings beat this quarter.

Investors are closely watching this report amid changing dynamics in the energy sector and recent gains in the company’s stock price.

Image Source: Zacks Investment ResearchForecasts: Revenue Dip, But Earnings GrowthAnalysts polled by Zacks have forecasted second-quarter revenues of approximately $5.06 billion for Constellation Energy, which would mark a 7.6% decline compared to the same quarter last year. Despite this drop in sales, earnings are expected to improve. The consensus estimate for earnings per share (EPS) stands at $1.83, signaling an 8.9% increase from the previous year.

Image Source: Zacks Investment ResearchHowever, it’s worth noting that this EPS estimate has edged slightly lower over the past 60 days, suggesting that analysts are cautiously adjusting expectations ahead of the report.Earnings Track Record: A Mixed BagOver the last four quarters, Constellation Energy has exceeded earnings expectations three times and met once. This track record has delivered an average earnings surprise of 7.41%, reflecting the company's ability to outperform in recent reporting periods.What the Quant Model Suggests

Despite the positive earnings growth outlook, Zacks’ proprietary model doesn’t strongly indicate that Constellation Energy will beat expectations this time around. A combination of a positive Earnings ESP (Expected Surprise Prediction) and a Zacks Rank of #1 (Strong Buy), #2 (Buy), or #3 (Hold) tends to boost the chances of an earnings beat. But in this case, Constellation has an Earnings ESP of 0.00% and currently holds a Zacks Rank #3 (Hold), which does not conclusively tip the odds in favor of a surprise.Sector Peers That Could Outperform

Investors seeking alternatives in the energy space might consider stocks like Permian Resources Corporation (PR), Talos Energy (TALO), and SolarEdge Technologies (SEDG). All three have positive Earnings ESPs—PR at +3.51%, TALO at +34.58%, and SEDG at +4.53%—and currently maintain a Zacks Rank #3. This combination boosts the probability of an earnings beat for these companies.Factors That May Have Driven Q2 Performance

Constellation Energy’s Q2 performance likely benefited from multiple operational tailwinds. Strong commercial execution, customer demand growth, and optimized energy portfolio management are expected to support earnings.

Image Source: Zacks Investment ResearchIts extensive nuclear infrastructure plays a key role in meeting the escalating electricity demands of data centers, likely driving revenue stability. The company’s active expansion into renewables, beyond its traditional nuclear focus, also positions it well for sustainable long-term growth.CEG’s emphasis on providing customer-centric, low-carbon solutions—such as carbon-free energy and renewable energy certifications—may further bolster profitability and appeal to clients aiming to reduce emissions and manage energy costs effectively.Stock Performance and ValuationIn the last three months, Constellation Energy shares have surged by 29.6%, outpacing the broader industry’s 23.9% gain. This strong rally, however, has pushed the stock to trade at a premium.

Image Source: Zacks Investment ResearchCEG’s forward 12-month price-to-earnings (P/E) ratio stands at 32.60x, well above the industry average of 22.24x, reflecting elevated investor expectations and a potential valuation concern for new entrants.Should Investors Buy, Hold, or Wait?Given Constellation Energy’s consistent growth strategies, expanding renewable portfolio, and solid execution, current investors may find it wise to hold the stock through the upcoming earnings report. However, for potential new investors, it may be prudent to wait until after the earnings release before initiating a position—especially considering the stock’s premium valuation and the lack of a strong signal for an earnings beat this quarter.